If you or your partner are struggling with debts, you may be able to reduce payments to an affordable amount in an IVA. Any remaining debts could be written off on completion. Fill in the form to find out your options.

Find out if an IVA is right for you

An Individual Voluntary Arrangement (IVA) is a formal debt solution between you and your creditors, that could help you deal with your unaffordable debts. In order to do an IVA, you first need to determine if it is a suitable option. There may be other debt solutions available to help you address your financial difficulties, so it is important that you are informed of all possibilites. If you wish to apply for an IVA, you will need the assistance of a professional called an Insolvency Practitioner or IP who will help set up your proposal and facilitate the agreement if it is approved by creditors.

In an IVA you could have:

In order to determine if an IVA is a suitable option, we must first run through some questions with you about your debts, income and household expenses. This will help us determine how much you can realistically afford to pay, whilst allowing for a reasonable standard of living. We will provide impartial advice, explaining all available options for dealing with your debts as it is possible that there are solutions available which you are unaware of, such as a Debt Management Plan, Debt Relief Order or Bankruptcy for example. Our advice will help you make an informed decision on how you would like to address your debts.

If you decide to apply for an IVA, then your proposal will be drafted with the help of one of our Insolvency Practitioners. It will be sent to you for review and to confirm that everything is correct. When you are happy with the proposal and everything has been explained in full, the proposal is sent to your creditors for voting. If more than 75% of your creditors (by debt value), vote in favour of the proposal, then your IVA is accepted and your payments can begin.

Your IVA will be supervised for it’s duration and regular reviews will be carried out to make sure your IVA is affordable, sustainable and fair for both you and your creditors. If you have any changes in your situation during the term of the IVA, you must notify your IVA provider, so that they can work with you to try and keep the IVA going wherever possible.

As an IVA is 'Individual', there is technically no such thing as a joint IVA, but if you and your partner both choose to do IVAs to address your debts, then you could apply for ‘Interlocking IVAs’. Interlocking IVAs are two IVAs that are linked and set up together at the same time. You both make one joint affordable payment each month that goes towards the linked IVAs.

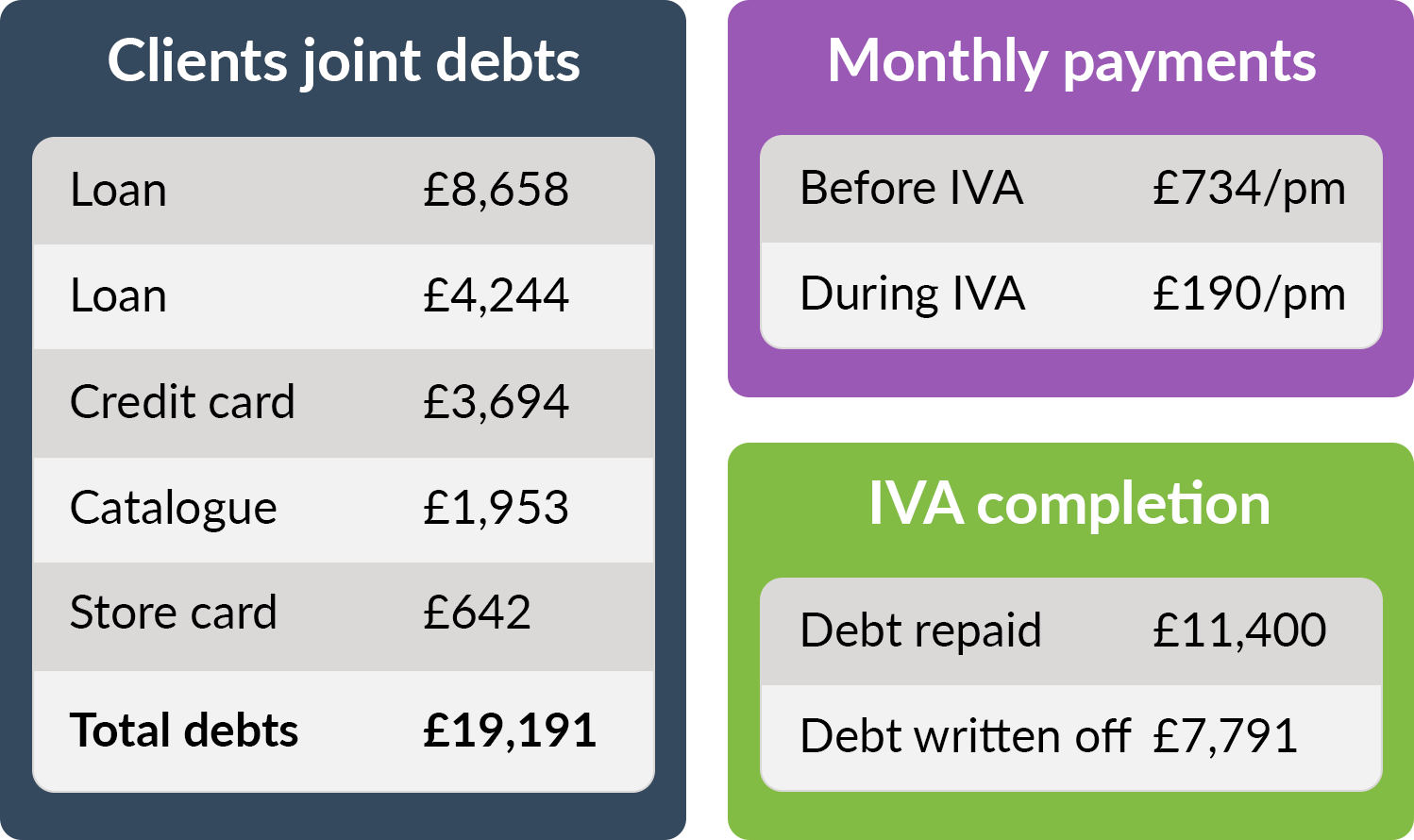

Total debts: £19,191

Total monthly repayments: £734

Client affordability (IVA payment): £190 per month

Debt Repaid in an IVA of 60 months: £11, 400

Debt Written off on successful completion: £7,791

* This is an example for demonstration purposes and is not a real IVA case. Figures are based on a standard IVA of 60 months, with payments remaining the same for the duration of the IVA and successful completion of the IVA.

The fees for an IVA are all set by the creditors (no matter which provider you use), so if your IVA application is successful, the only thing to worry about is whether you have chosen the right Insolvency Practitioner or not.

All fees are taken out of your affordable monthly payment so you will never be asked for additional fees or receive a bill from us.

We work very hard to get your IVA accepted, but if for any reason your creditors do not accept your IVA proposal, we charge nothing whatsoever.

Yes, but not forever. Whilst you are in an IVA, you will understandably not be able to obtain credit of any sort and you will have to give up any existing credit that you have. This continues until your IVA is complete. So, you can work on rebuilding your credit rating after your IVA has completed.

f you’d like more information on other sources of free debt help and advice you can visit MoneyHelper – an organisation, backed by government and set up to offer free and impartial advice to those in debt. - Click here to visit MoneyHelper

We are happy to provide you with debt advice only. We only charge a fee if you opt for one of our debt solutions. Fees will depend on which debt solution we provide and what your personal circumstances are. All fees will be discussed prior to commencement of any service or debt repayment plan. Click here to read our fees and key info Please note: From time to time we may refer you to other services providers or charities such as the CAB.

At National Debt Relief we prioritise the customer experience above all else. We are commited to going above and beyond in meeting customer expectations and believe in caring, listening and understanding your needs, especially when it comes to discussing the stressful situation of unaffordable debt. We believe our attentive customer service is reflected in the feedback we receive from our clients. Below, you can read what some of our clients think of the services we offer. All reviews are collected on Independent review site TrustPilot. If you have any questions at all, please get in touch. You can pick up the phone and call us on 0800 888 666 0 or click here to drop us a message on WhatsApp.

We are authorised and regulated by the Financial Conducty Authority (FCA) to provide debt advice.

We are duty bound to advise you on ALL options available for your situation.

If you're not sure of all of your outstanding debts, we can help with this.

You could lower unaffordable monthly payments with an informal or formal debt solution.

You may be eligible able to write off unaffordable debt with a formal solution.

We are a family run company, who pride ourselves on our friendly caring approach.

We have good creditor relationships, which helps us get the best plan for you.

All advice we provide is free and confidential. You are under no obligations by contacting us.